Financing Prompts Are Everywhere. Here’s Why.

Photo credit: Ivan S/Pexels.com

Everywhere you turn, someone is offering to slice your purchase into smaller payments. From checkout buttons on $100 sneakers to point-of-sale pitches for HVAC repairs, financing has shifted from a rare tool to a default part of how you shop. You are not imagining it: the prompts to “split it up” are multiplying because they solve problems for stressed consumers and hungry businesses at the same time.

To understand why these offers feel inescapable, you have to look at the collision of economic strain, new financial technology, and a culture that has grown comfortable living on tomorrow’s money. Once you see how those forces fit together, the constant nudges to finance almost everything stop looking like a quirk of modern retail and start to resemble a new operating system for your financial life.

The economic pressure that makes financing feel like a lifeline

You are being targeted with more financing options in part because your budget is under strain. Research on household finances shows that 67% of Americ are living paycheck to paycheck, a jump from the prior year that reflects higher costs and uneven wage growth. When two thirds of people have little cushion, the promise of spreading a bill over time, instead of paying in full today, becomes an easy sell.

That pressure also changes how you plan. Analysts tracking consumer behavior describe a rise in Reactionary Approaches, with most Americans now classified as reactors who respond to financial stress in the moment instead of following a long term plan. When you are reacting, not strategizing, a financing prompt at checkout can feel like a quick fix rather than another obligation. Companies understand this, which is why you see offers to “pay later” embedded in everything from online carts to medical bills.

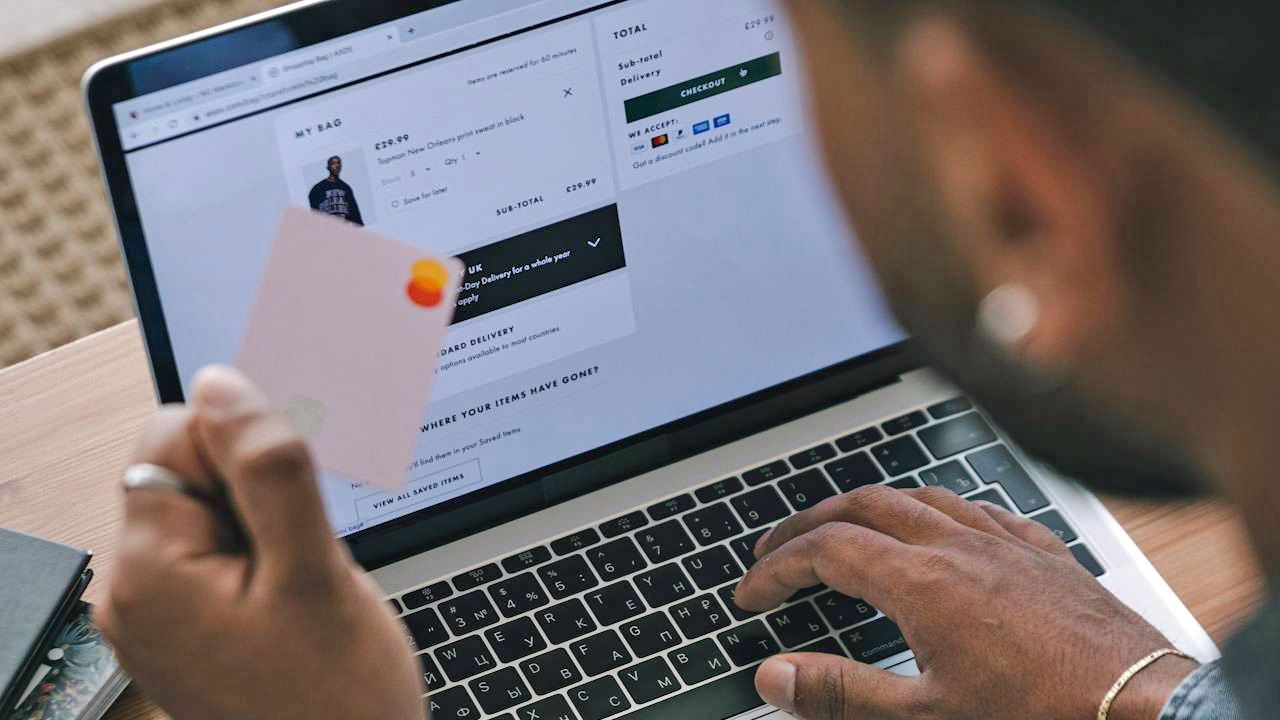

How Buy Now, Pay Later turned checkout into a credit decision

The most visible face of this shift is Buy Now, Pay Later, often shortened to BNPL. Instead of applying for a traditional credit card, you tap a button from providers like Klarna and Affirm and split a purchase into a handful of installments. With this model, you can buy something before putting a dime down, which can feel enticing if you are juggling bills or trying to stretch a tight month.

Unlike older layaway programs, Buy Now, Pay Later lets you walk away with the item immediately while a third party lender such as Klarna, Afterpay or Affirm fronts the money and collects your payments over time. At checkout, you might see a message that a $100 item can be yours for four smaller payments, reframing the decision from “Can I afford this total?” to “Can I handle this slice?” Because the process is so quick and often marketed as interest free, it can be easy to forget that you are taking on a loan.

Why retailers are pushing financing so aggressively

From the merchant’s perspective, financing prompts are not a courtesy, they are a growth strategy. When you accept an offer to split a bill, you are more likely to complete the purchase and to spend more overall. Providers of point of sale financing software highlight that when customers have more time to pay, They can afford higher priced products and services, which in turn lifts average order value and can generate a reported 726% return on investment for retailers that integrate these tools.

Smaller businesses are being sold the same promise. Guides aimed at local merchants emphasize that offering financing can lead to Increased Sales and Average Order Value Higher, because Customers are more likely to say yes when they can spread payments out. In home services, industry playbooks argue that Modern consumers have grown accustomed to financing in nearly every category, so presenting monthly payment options for things like plumbing repairs or roof work has become an expectation rather than a luxury. When financing boosts conversion rates and ticket sizes, it is no surprise that you see it everywhere from furniture showrooms to dentist offices.

The tech that makes “pay later” feel frictionless

The explosion of financing prompts is also a story about software. A decade ago, applying for credit meant filling out forms and waiting for approval. Now, a few taps on your phone can generate an instant decision at checkout. Commentators who track the sector point out that the technology behind Buy Now, Pay Later is nimble and fast, which is why you can be approved in seconds while shopping online or in a store. That speed is part of the appeal, but it also means you can stack multiple loans before you have fully processed what you owe.

Some observers note that these services often skip traditional credit checks or use lighter versions, which makes them accessible to people who might not qualify for a card but also raises concerns about overextension. One discussion of the unregulated boom in this market highlights that the reason these products spread so quickly is that they are just so easy to use, with a few quick taps or clicks, and that And the providers do not always vet borrowers the way banks do. When the barrier to borrowing is that low, the natural result is more prompts, more approvals, and more people juggling overlapping payment plans.

The psychological pull of “small payments”

Financing prompts work on your emotions as much as your spreadsheet. Behavioral researchers and personal finance coaches see a pattern: when you are shown a small installment instead of a full price, your brain tends to focus on the immediate, manageable number. In one conversation about debt, a shopper describes buying a $100 pair of shoes and feeling as if the shoes cost $25 because that is all they had to pay that day, even while carrying $107,000 in total debt. That mental framing is exactly what makes installment offers so powerful.

Digital tools can either reinforce or challenge that mindset. One writer who turned an AI system into a personal finance coach describes how the tool flagged their worst money habits by analyzing spending patterns and recurring subscriptions. Other creators share multi stage prompts designed to expose hidden money blocks, with instructions like How To Use and reminders to ONLY adjust a parameter labeled Share your honest situation and to answer questions such as What type of financial stress you are facing. These experiments show that the same AI techniques used to make financing offers smarter can also be used to help you see through the allure of “bite sized” payments and confront the full picture of your obligations.

When convenience turns into hidden risk

For all the convenience, the spread of financing into every corner of your life carries real risk. Analysts warn that Buy Now, Pay Later services have ballooned, with companies like Klarna and Affirm enabling people to break up purchases into small chunks that can quietly pile up. Because many of these loans are not reported the same way as credit cards, it can be harder for you, and sometimes for lenders, to see the total exposure until a payment is missed.

Consumer advocates point out that nearly 1 in 4 Americans using these products are at risk of falling behind, in part because the ease of approval and lack of upfront interest charges can mask the true cost. Traditional lenders are starting to respond with AI powered coaching that offers Quality advice at scale, with systems that can walk you through the exact steps needed to improve your credit scores after a decline. Yet those tools are still catching up to the speed at which new financing options are being pushed, which leaves you responsible for tracking how many “later” payments you have promised your future self.

How AI and prompts are reshaping your money decisions

Behind the scenes, the same AI that powers chatbots is increasingly steering financial choices. Corporate finance teams are being told that Most of them are using Chat GPT for only a fraction of what it can do, and that You are wasting at least an hour a day if you limit it to drafting emails instead of using it as a second brain for analysis, procedures, tools, and problem solving. That mindset is spilling into consumer products, where AI engines can analyze your accounts, predict cash flow, and surface tailored offers, including financing, at the exact moment you are most likely to accept.

Financial advisors are also being coached on AI Prompting 101 so they can ask better questions of these systems and deliver more personalized guidance. Some banks are experimenting with AI powered coaching that can rival what the best human advisors provide, using Today’s engines to generate step by step plans after a credit decline. As these tools mature, you can expect more prompts that do not just ask whether you want to split a purchase, but that nudge you toward or away from certain choices based on your history, your goals, and even your emotional patterns around money.

Why financing now feels like the default, and how to respond

Put together, these trends explain why financing offers feel omnipresent. You are living in an economy where 67% of Americ are stretched, where Reactionary Approaches are common, and where retailers have learned that embedding credit at the point of sale reliably boosts revenue. Providers like Klarna and Affirm have turned Buy Now, Pay Later into a standard checkout feature, while software platforms promise merchants that They will see higher order values and strong returns if they add more ways for you to pay over time.

That does not mean you have to accept every prompt. You can treat each offer as a small credit decision and run it through the same filter you would use for a loan: Do you understand the total cost, the schedule, and what happens if you miss a payment? You can also enlist the same AI tools that marketers use, from personal finance coaches that flag your weak spots to structured prompts that help you Share your honest situation and clarify What you really want your money to do. In a world where financing is everywhere, your edge is not avoiding the prompts altogether, it is learning to see through the design and choose when borrowing truly serves you instead of the other way around.